LMI Waivers for Medical Professionals: 2026 Guide

How doctors, nurses and allied health professionals can avoid Lenders Mortgage Insurance, who qualifies, and where the policies actually differ between lenders.

LMI Waivers for Medical Professionals in Australia: The 2026 Guide

Lenders Mortgage Insurance is the single largest avoidable cost in an Australian home purchase. On a million-dollar property at 90% LVR, the premium can comfortably exceed $20,000. At 95% LVR, it can push past $40,000. None of that money goes towards your home equity, your offset account, or your retirement. It sits with the lender as a risk hedge, paid in full by you.

For most borrowers, that cost is unavoidable below a 20% deposit. For medical professionals, it often is not. A range of Australian lenders waive LMI entirely for eligible doctors, nurses, allied health workers and other healthcare roles, sometimes at LVRs as high as 95%. The reasoning is simple: medical professionals have lower default rates and more stable long-term income trajectories, so lenders treat them as a desirable banking relationship and price the risk accordingly.

The catch is that policies vary substantially between lenders. A registered nurse may be told at one major bank that they don’t qualify for any waiver, while a competitor across the street offers 90% LVR with no LMI on the same loan. A physiotherapist might be quoted $18,000 in LMI at one lender and zero at another. Whether you save tens of thousands of dollars or pay the full premium often comes down to which lender you walk into.

This guide walks through how LMI waivers work for medical professionals in Australia in 2026, who qualify, the differences between lender policies, and the questions worth asking before you apply.

What is an LMI Waiver?

Lender's Mortgage Insurance is a one-off premium charged by the lender when a borrower takes out a loan above 80% of the property’s value. Despite the name, it does not insure the borrower — it insures the lender against the borrower defaulting. The premium scales with both loan size and loan-to-value ratio, and is typically capitalised onto the loan, meaning you also pay interest on it for the life of the loan.

An LMI waiver is exactly what it sounds like: the lender drops the requirement entirely for borrowers who meet certain professional criteria. It is not a discount, a refund, or a rebate — the premium is simply not charged. Your loan amount stays the same; the LMI line item just disappears.

That means a 95% LVR home loan for a doctor can cost the same upfront fees as an 80% LVR loan for someone else, while requiring less than half the deposit. In practice, this opens up three pathways that are not realistically available to non-medical borrowers:

- The smaller-deposit pathway: keep more of your savings invested or in offset, and buy with as little as 5% deposit while avoiding the insurance hit.

- The earlier-purchase pathway: buy years before you would otherwise have saved a 20% deposit — a meaningful advantage in markets where prices are rising faster than savings.

- The larger-property pathway: the same deposit funds a more expensive purchase, because you’re borrowing at a higher LVR without the premium penalty.

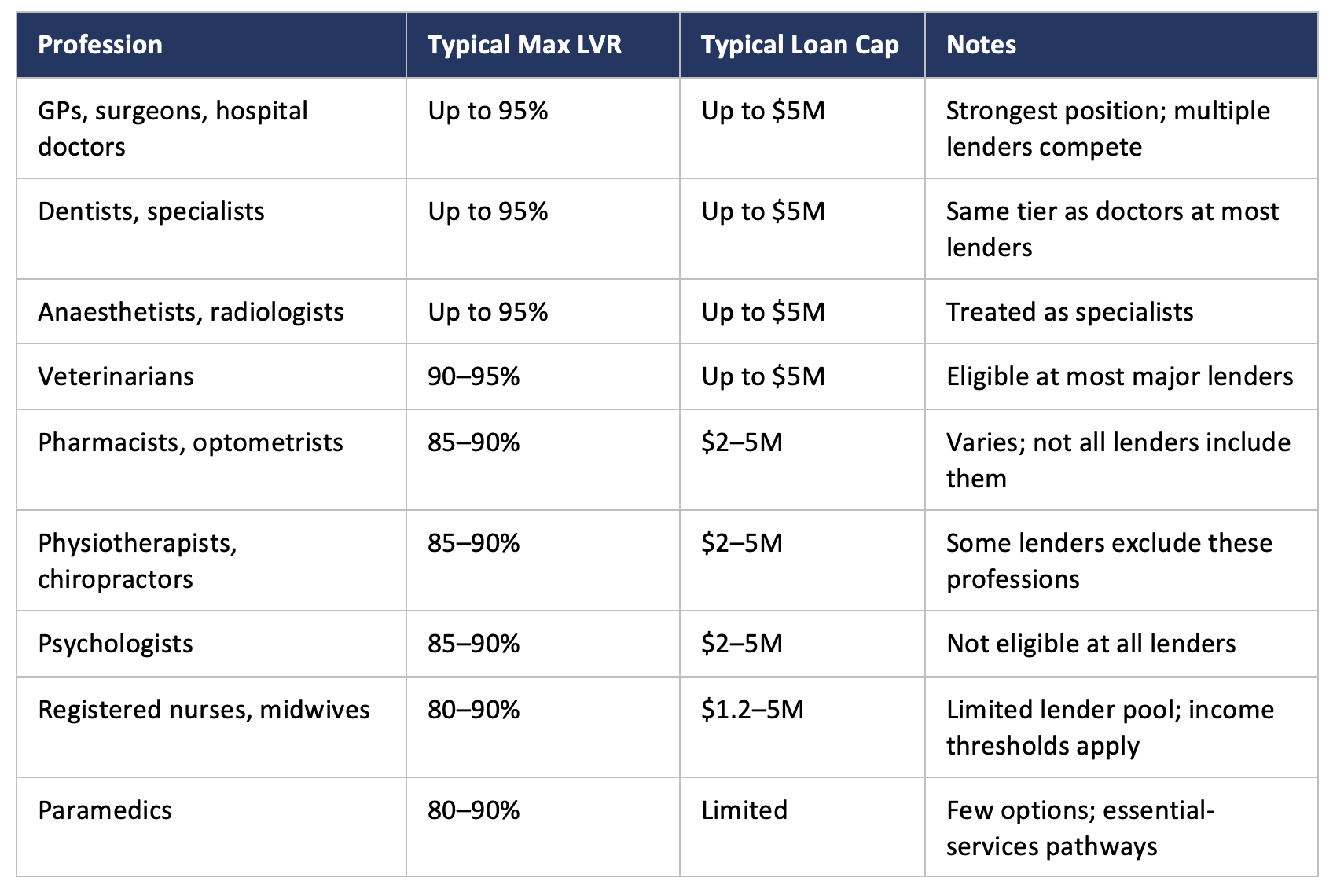

Who Qualifies: A Quick Reference by Profession

The headline benefits available to medical professionals across major Australian lenders break down roughly as follows. Specifics shift regularly as lenders update their policies, so this should be treated as directional rather than definitive.

The two takeaways: doctors, surgeons and dentists have the broadest range of options and the most competitive terms, while nurses and paramedics have a narrower lender panel — but real options exist if you know where to look.

Doctors, Surgeons and Dentists

Registered medical practitioners — GPs, hospital doctors at any career stage from intern through staff specialist, surgeons, anaesthetists, dentists, and recognised specialists — sit at the top of the LMI waiver tier. Several major lenders offer up to 95% LVR with no LMI for owner-occupied purchases, with loan sizes typically capped at around $5 million per security and group exposure caps of around $7.5 million across the lender’s banking group.

A few practical points worth knowing:

- The waiver is profession-based, not seniority-based. An intern starting their hospital rotation can access the same headline LVR as a 20-year specialist. Borrowing capacity differs, but the LMI waiver itself does not.

- Self-employed practitioners (private GPs, specialists, dentists with their own practice) face additional documentation, but several lenders accept a single year of tax returns rather than the standard two, recognising that practice income often grows quickly.

- Loans can usually be held in your own name or via related company or trust structures, provided you have direct ownership or directorship.

- Hospital-employed doctors with significant overtime,on-call and shift allowances may have those amounts assessed at 100% under some lenders’ policies. For early-career doctors, where these payments can exceed $40,000–$60,000 per year, this can lift borrowing capacity by hundreds of thousands.

Pharmacists, Optometrists and Veterinarians

A second tier of medical professions also receives strong treatment, though specifics vary more lender by lender. Optometrists, pharmacists, podiatrists, audiologists, sonographers, speech pathologists, radiographers, and veterinary practitioners are eligible for LMI waivers with multiple major lenders, typically at 90% LVR and with loan caps similar to those for doctors.

The key difference is income thresholds. Several lenders apply a minimum gross income requirement (often around $90,000) for these professions to qualify, whereas doctors have no such floor. For full-time practitioners, this is rarely an issue, but it can affect part-time workers or those returning from career breaks.

Veterinarians are worth a specific note: they are well-treated by most lenders with medical professional policies — including the major banks — even though “veterinary practitioner” sometimes feels like an afterthought in policy documents. If you’re a vet, do not assume you’re excluded just because the marketing imagery shows stethoscopes.

Allied Health: Physiotherapists, Chiropractors, Psychologists

Allied health is where lender policies diverge most. Physiotherapists, chiropractors, psychologists, osteopaths and similar professions have meaningful LMI waiver options available, but the lender panel narrows significantly.

Some major banks include allied health in their specialist policies. Others explicitly exclude physiotherapists or psychologists from the medical professional pathway entirely, treating them as standard borrowers. The practical effect is that an allied health professional walking into the wrong bank may be quoted full LMI on a 90% LVR loan, while a different lender across the street would waive it entirely — same income, same loan size, same property.

A typical allied health LMI waiver typically includes a 90% LVR, a minimum income threshold (often $90,000 from the eligible profession), AHPRA registration in the relevant category, and standard serviceability tests. The application requirements are not dramatically different from a standard home loan — the policy framework is what changes.

Nurses, Midwives and Paramedics

Nursing and paramedicine are the most challenging categories to place, but there are real options.

For registered nurses and midwives, several lenders offer 90% LVR with no LMI, typically with a minimum income threshold from the eligible profession. The lender panel is narrower than for doctors — only a handful of mainstream lenders extend the waiver to nurses, while most major banks exclude them entirely. That said, the lenders who do offer nurse waivers tend to be competitive, and the policies have generally become more inclusive over the past few years rather than less.

Paramedics face the tightest pool. A small number of lenders include paramedicine within their medical professional waiver structure, often via AHPRA Paramedicine Board accreditation. A separate “essential services” pathway is offered by some lenders, extending similar treatment to paramedics, registered nurses, and police, with smaller loan caps but workable terms for typical first home purchases.

A Worked Example: How Much Does the Right Lender Save?

Consider Sarah, a registered nurse in her early thirties, earning $98,000, looking to buy her first home for $720,000 with a $50,000 deposit (around 7%).

At a major bank where nurses are excluded from the specialist policy, Sarah is quoted Lenders Mortgage Insurance of approximately $24,000, which is added to her loan, increasing her debt and interest costs over the life of the loan.

At a lender that includes nurses in its medical professional waiver, the same purchase at 93% LVR is approved with no LMI charged. Sarah’s loan stays at $670,000 instead of $694,000. Over a 30-year term, this saves her not just the $24,000 in upfront fees but also approximately another $25,000 in interest costs over the life of the loan — a total saving of over $49,000 from a single policy difference.

The application required the same documents, the same serviceability assessment, and the same approval timeline. The only difference was knowing which lender to approach.

How an LMI Waiver Application Works

The documentation requirements for a medical professional home loan are not dramatically different from a standard application, but a few extras apply.

If you’re employed (PAYG)

Recent payslips, group certificates or income statements, employment contract or letter confirming your role and registration, AHPRA registration printout, and bank statements showing salary credits. If you receive significant overtime,on-call or shift allowances, three months of payslips help establish a pattern.

If you’re self-employed

At least one full year of tax returns and notice of assessment, financial statements for any associated entities (company, trust, partnership), AHPRA registration, and current bank statements for business and personal accounts. Two years of returns is more typical, but specialist medical professional lenders often accept one year — a meaningful advantage for those who have recently transitioned to private practice.

AHPRA registration

Universal across every lender with a medical professional waiver. General registration is fine for most professions; some specialist registrations are also accepted. Student and non-practising registrations are generally not eligible.

Investment property purchases

Add rental income evidence (existing tenants) or a market rent appraisal (new purchases), plus details of any existing investment property holdings. Investment LVR caps are typically 90% rather than 95%.

Common Pitfalls and What to Watch For

Even when a waiver is technically available, a few situations regularly cost medical professionals money or kill the application altogether.

- Walking into one bank and assuming the answer is the answer. The single biggest mistake is treating one lender’s policy as representative of the market. Policies vary widely across lenders, so a flat decline at one bank often coexists with a 95% LVR approval at another.

- Multiple credit enquiries from shopping around.Applying to several lenders in sequence stacks credit enquiries on your file, which itself becomes a flag for later applications. Working with a broker avoids this; doing it yourself across multiple banks does not.

- Missing the income-threshold floor. For allied health and second-tier professions, the $90,000 minimum income from the eligible role is a hard cut-off at many lenders. Combining household income with a non-medical partner’s salary doesn’t always count toward this threshold.

- Confusing general registration with practising registration. A non-practising AHPRA registration usually fails the eligibility test even if your other documents are in order.

- Treating overtime and on-call income as bonus pay. At lenders that don’t have specialist policies, hospital allowances may be discounted or excluded from serviceability, dropping borrowing capacity by tens or even hundreds of thousands. Specialist medical lender policies often assess this income differently.

Frequently Asked Questions

Can I get an LMI waiver as a hospital doctor on a graduate salary?

Yes. Most major Australian lenders with medical professional policies treat all registered medical practitioners equally on the LMI waiver, regardless of seniority. Your serviceability and borrowing capacity will reflect your current income, but the LMI waiver itself does not require minimum experience or seniority for doctors.

Are nurses eligible for the same LMI waivers as doctors?

Not at all lenders. Several major banks exclude nurses from their medical professional waiver policies. However, a smaller number of lenders include registered nurses and midwives at up to 90% LVR with no LMI, typically with a minimum income threshold.

What is the maximum loan size under a medical professional LMI waiver?

Loan caps vary by lender, but most major lenders cap medical professional waiver lending at around $5 million per security, with aggregated exposure caps of $7.5 million across the broader banking group. Larger loans are possible but generally fall outside the standard waiver structure.

Can the waiver be used on an investment property?

Yes, though terms differ. Investment purchases are typically available at 90% LVR with no LMI for eligible medical professionals, compared to 95% LVR for owner-occupied properties. A few lenders offer specific investment-only waivers for doctors at higher LVRs.

Do I need to be self-employed, or does it work for hospital-employed staff?

Both are eligible. Hospital-employed doctors and PAYG-employed nurses, allied health and other medical professionals, all qualify under the same policies as self-employed practitioners. Documentation differs (payslips and income statements vs. tax returns and financials), but the LMI waiver itself is not dependent on the employment structure.

How long does the application take?

Typical medical professional applications take two to four weeks from submission to formal approval, with another two to six weeks to settlement, depending on the property purchase. Some lenders offer faster pre-approval pathways for established medical clients.

What if I’m part-time or on parental leave?

Part-time and reduced-hours medical professionals can still access most LMI waivers, though serviceability assessment will reflect actual income. For those on parental leave, several lenders accept return-to-work letters as evidence of resumed income, allowing applications to proceed.

Are there medical professions that don’t qualify anywhere?

A small number of allied health roles (such as dental therapists, hygienists and dental assistants) are typically excluded from medical professional waiver policies at all major lenders, and treated as standard borrowers. If your role sits in this space, the LMI waiver pathway may not be available, but standard high-LVR lending with LMI remains.

Where to Go From Here

LMI waivers for medical professionals are one of the most valuable concessions in Australian residential lending, but the value only materialises when you find the right lender for your specific profession, income mix and entity structure. The same applicant can receive a 95% LVR no-LMI offer at one lender and a flat decline at another — not because the borrower changed, but because the policy did.

If you’re weighing up your options, the most useful next step is to get a clear picture of which lenders currently extend the waiver to your specific profession at your specific income level. Mortgages Plus works with more than 50 Australian lenders and tracks medical professional policies as they evolve. We’re happy to walk you through what’s realistically available for your situation, with no obligation and no fee — brokers are paid by the lender at settlement.

Visit mortgages-plus.com.au or get in touch directly to start the conversation.