Northern Beaches Property Prices Guide

A 2026 guide to Northern Beaches property prices, growth trends, and home loan insights. Explore suburb-by-suburb medians, investment opportunities, and borrowing strategies across one of Sydney’s most in-demand, supply-constrained markets.

Northern Beaches Property Prices 2026: A Suburb-by-Suburb Guide to Medians, Growth & Home Loan Insights

Sydney’s Northern Beaches is one of Australia’s most sought-after property markets as well as one of its most nuanced. Median house prices in 2026 range from the low $2 millions in the Warringah hinterland to more than $5 million in the premium pockets of Balgowlah Heights, while the unit market spans entry-level Brookvale apartments at around $1 million up to Manly and Fairlight stock above $1.8 million.

If you’re buying, refinancing, or building an investment portfolio along the 30 kilometres of coastline from Manly to Palm Beach, understanding suburb-level pricing and how it translates into borrowing power is the difference between stretching your budget and buying well. At Mortgages Plus, our local brokers arrange NorthernBeaches home loans every week, and this 2026 guide distils what we see in the market into one place: suburb medians, one- and five-year growth, rental yields, vacancy rates, borrowing-capacity examples, and the infrastructure pipeline that is likely to move prices over the next few years.

The Northern Beaches market at a glance (2026)

• Population: ~270,000 residents today, forecast to reach 313,000 by 2041 (Northern Beaches Council)

• Home ownership: 68% of households own or are buying their home

• Gross Regional Product: more than $21 billion, anchored by health, professional services, construction, retail and tourism

• Median house price range: $2.1M (North Narrabeen) to $5.01M (Balgowlah Heights)

• Median unit price range: $1.00M (Brookvale) to $1.85M (Fairlight)

• Rental vacancies: below 1% in most suburbs, with the tightest markets at Mona Vale, North Narrabeen and Narrabeen (0.2–0.3%)

• Long-term growth: most suburbs have averaged 7–9% annual house price growth over the past five years

Sources: PropTrack, Northern Beaches Council, Hotspotting Summer 2026 Price Predictor Index, 2021 ABS Census.

Why the Northern Beaches keeps outperforming

Three forces are driving persistent buyer demand: lifestyle, limited supply and infrastructure investment.

Lifestyle: more than 20beaches, Ku-ring-gai Chase National Park on the doorstep, and the Spit-to-Manly and new 36 km Palm Beach-to-Manly Coastal Walk mean this is Sydney’s most walkable coastline. Tourism alone generated $2.996 billion in visitor expenditure in FY2024.

Supply constraints: the peninsula is physically bounded by water and a national park, and building approvals have trended downward since 2017–18, when more than 1,100 dwellings were approved. In 2024–25, approvals fell to around 230 houses and 235 units, meaning demand continues to outstrip new stock.

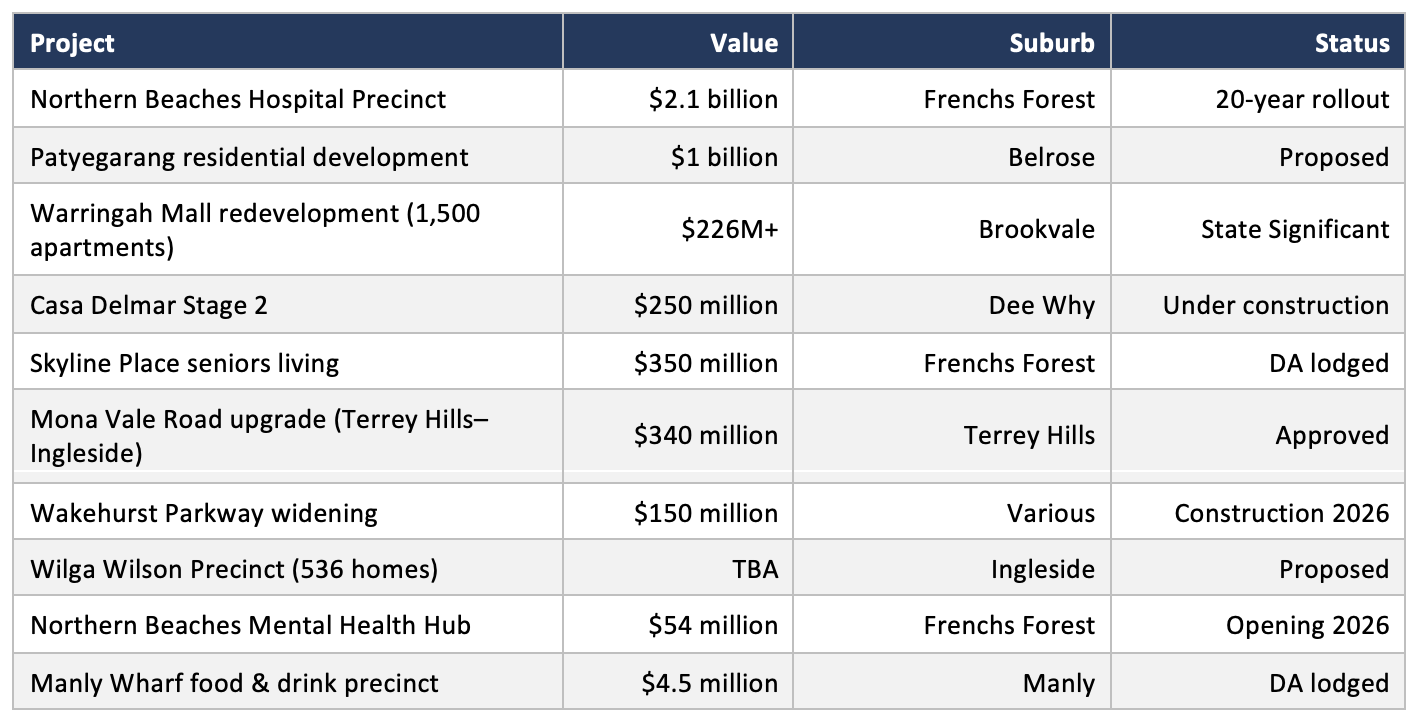

Infrastructure: the NSWGovernment and Northern Beaches Council have more than $2 billion in committedand planned projects, including the $2.1 billion Northern Beaches HospitalPrecinct at Frenchs Forest, the $340 million Mona Vale Road upgrade, the $150million Wakehurst Parkway widening, and the Low and Mid-Rise Housing policythat is unlocking denser development around nine town centres including Manly, Balgowlah, Dee Why, Mona Vale and Brookvale.

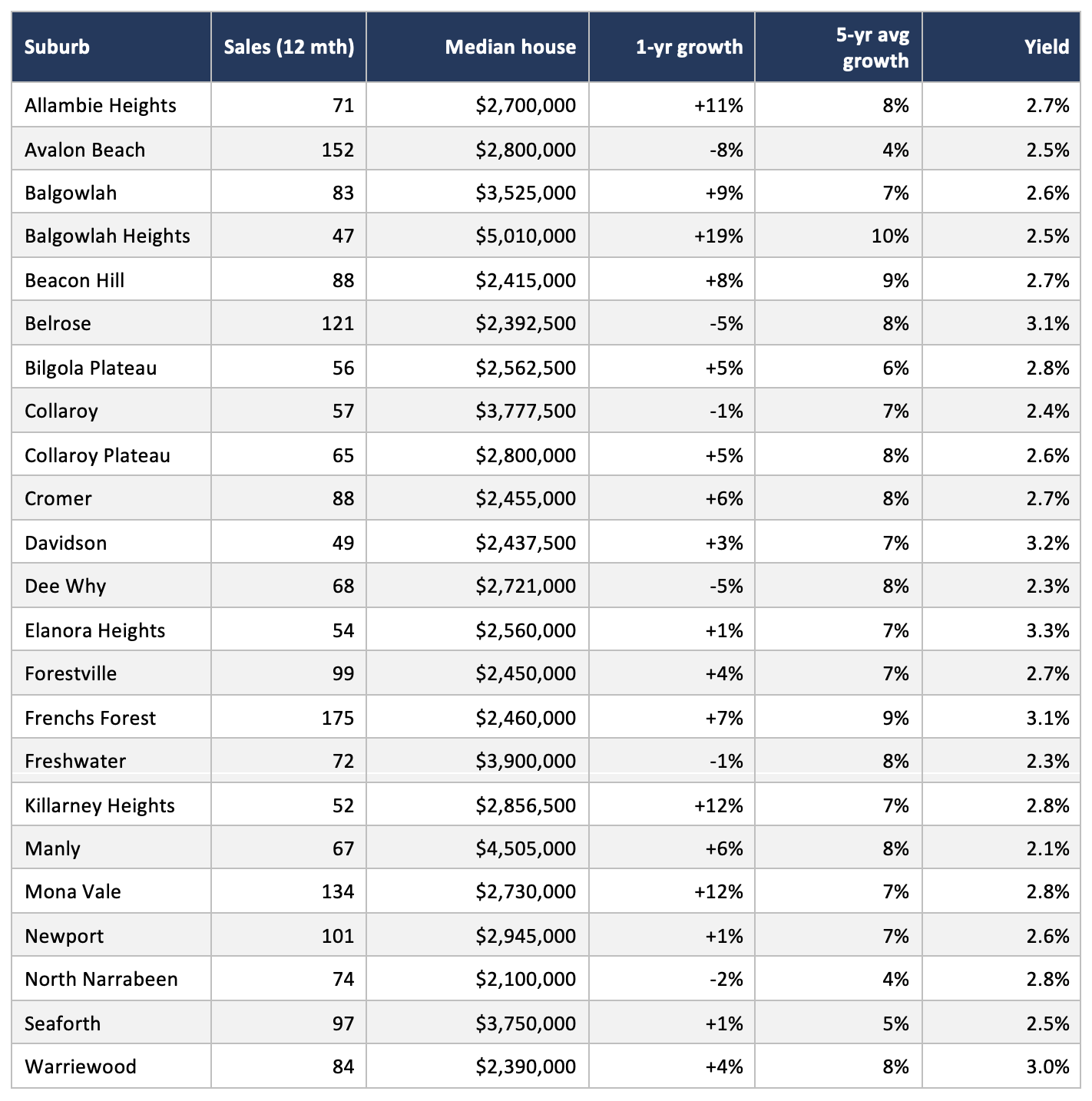

Northern Beaches house prices by suburb (12 months to Jan 2026)

The table below compares every major Northern Beaches suburb by median house price, one-year growth, five-year average annual growth, and rental yield. Use it as a starting point and then talk to a Mortgages Plus broker about which suburbs fit your borrowing capacity.

Source: PropTrack, 12 months to January 2026.

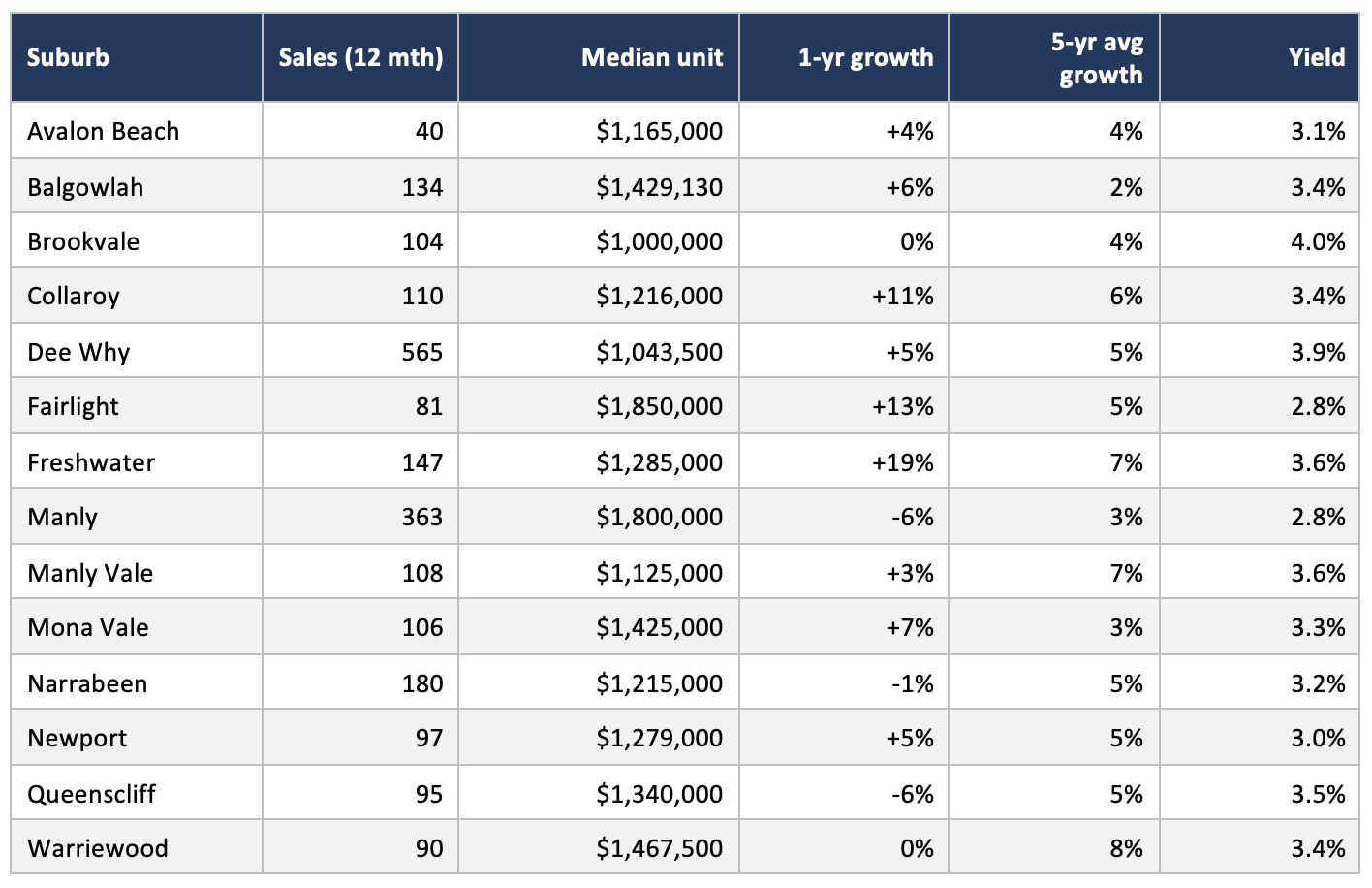

Northern Beaches unit prices by suburb (12 months to Jan 2026)

Units remain the most accessible entry point to the Northern Beaches. The 2026 Price Predictor Index shows 67%of Greater Sydney unit markets recording positive rankings, with standout Northern Beaches performers including Freshwater, Fairlight and Collaroy.

Source: PropTrack, 12 months to January 2026.

Suburb spotlight: where the opportunities are in 2026

Manly, Fairlight & Queenscliff — the premium gateway

Manly’s median house price sits at $4.505 million, with house values up 6% over the past year and averaging 8% growth annually over five years. The unit market is deeper — 363 sales in the past 12 months at a median of $1.8 million — and dominated by 25–45-year-old professionals, more than half of whom rent. A 20-minute ferry to Circular Quay keeps demand structurally strong.

Fairlight units are the quiet outperformer: up 13% year-on-year to a median of $1.85 million with a vacancy rate of just 0.4%. Queenscliff offers similar beachside access at a median unit price of $1.34 million.

Broker insight: Manly’s slow rental yields (2.1% houses) mean pure cash-flow investors often look further north. But for owner-occupiers and high-income professionals, Manly remains the benchmark. Expect lenders to scrutinise servicing closely at these price points — we routinely negotiate sharper rates for loans above $2 million.

Dee Why, Collaroy & Narrabeen - the value coastline

Dee Why is the Northern Beaches’busiest apartment market, with 565 unit sales in the past year at a median of $1.043 million (up 5%) and a 3.9% yield — one of the strongest rental returns within an easy walk of the beach. House prices sit at $2.721 million and, while they dipped 5% this year, the five-year average growth of 8% tells the longer-term story.

Collaroy units gained 11% over the year to $1.216 million; Narrabeen units are tightly held, with a 0.2% vacancy rate.

Broker insight: Dee Why is where we see the most first-time Northern Beaches buyers. The $250 millionCasa Delmar development (280 residences) and the adjacent $75 million Delmar Stage 1 are adding high-quality stock — useful if you’re considering off-the-plan, but be aware lenders apply valuation discounts on off-the-plan purchases, so deposit requirements can stretch.

Mona Vale, Newport, Avalon & Palm Beach - the Pittwater end

Mona Vale house prices grew 12% in the past year to $2.73 million, supported by major retail and health recent contrarian story — house prices fell 8% to $2.8 million over the year, infrastructure, while the unit market is posting a 7% gain to $1.425 million.Newport houses sit at $2.945 million with rents up 8% to $1,400 per week.

Avalon Beach is the market’srecent contrarian story - house prices fell 8% to $2.8 million over the year and the suburb appeared on Hotspotting’s Bottom 50 watchlist. However, the unit market at Avalon lifted 4% to $1.165 million with a 3.1% yield, and long-term five-year growth still averages 4% per year for houses.

Broker insight: Softer medians in Avalon can create buying windows for patient purchasers -particularly upgraders using equity in more central suburbs. If you’re bridging from an existing Northern Beaches home, bridging finance and cross-collateralisation structures are worth discussing carefully.

Frenchs Forest, Belrose, Forestville & Davidson - the growth corridor

This is where the next five years of structural change are concentrated. Frenchs Forest is an NSW Government Priority Planned Precinct, with 2,000 new homes earmarked around the Northern Beaches Hospital, $500 million in road upgrades, and major developments including the $350 million Skyline Place seniors project and a $71 million,124-apartment development opposite the hospital.

Frenchs Forest houses grew 7% to a median of $2.46 million, with an average annual growth of 9% over five years and a vacancy rate of just 0.8%. Belrose is the site of the $1 billion Patyegarang development (450 dwellings) by the Metropolitan Local Aboriginal Land Council.

Broker insight: Infrastructure-led growth corridors historically reward buyers who get in ahead of the construction phase. Investors considering Frenchs Forest should weigh the yield premium (3.1%) and tight vacancy against the lead time on major projects like the new town centre.

Balgowlah, Seaforth & Clontarf - the prestige harbourside

Balgowlah Heights is the LGA’s priciest suburb at a $5.01 million median, up 19% year-on-year and averaging10% annual growth over five years. Balgowlah ($3.525 million, +9%) and Seaforth($3.75 million, +1%) offer the same harbour access with slightly more family-sized stock.

Broker insight: Loans above $3 million often benefit from private bank pricing, offset-sweep structures, and interest-only periods for owner-occupiers. Mortgages Plus regularly benchmarks the major banks against private bank desks at these price points.

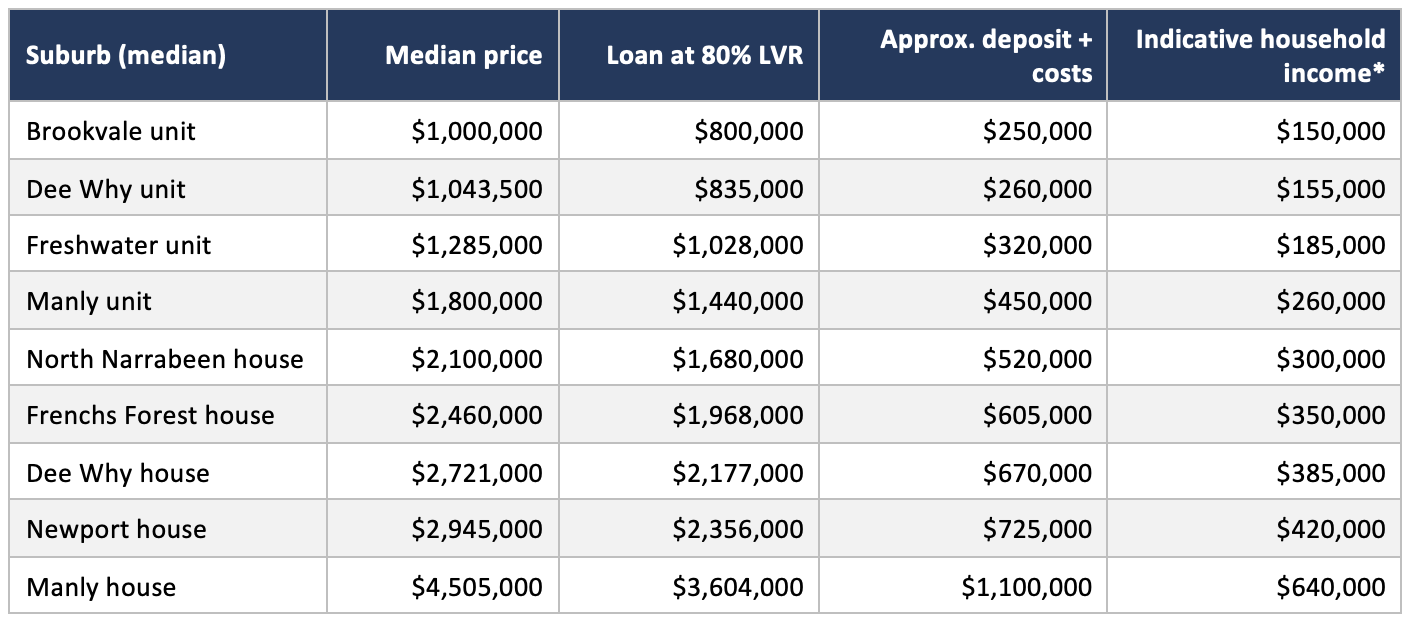

How much do you need to earn to buy on the Northern Beaches?

Borrowing capacity is the single biggest constraint for most Northern Beaches buyers. APRA requires lenders to assess loans with a serviceability buffer of 3 percentage points above the actual interest rate, which significantly compresses borrowing power in a higher-rate environment.

The indicative table below shows the approximate household income required to borrow the amount needed to purchase at each suburb’s median price, assuming a 20% deposit and standard principal-and-interest home loan terms. These are indicative only — actual capacity depends on expenses, dependants, debts, credit card limits, and lender policy.

*Indicative only. Based on a dual-applicant household with nodependants, minimal debts, and current owner-occupier P&I rates plus the 3%APRA serviceability buffer. Stamp duty, LMI, and purchasing costs included in the deposit estimate. Contact Mortgages Plus for a personalised borrowing assessment.

First home buyers on the Northern Beaches

Yes, it is still possible to buy your first home on the Northern Beaches in 2026 - but the strategy matters. For buyers using the NSW First Home Buyer Assistance Scheme (stamp duty concessions) and the Commonwealth First Home Guarantee (5% deposit without LMI for eligible first home buyers), the following suburbs offer stock near the relevant property price caps:

• Brookvale units: median $1.0 million — within reach of the NSW First Home Buyer Assistance concessional threshold.

• Dee Why units: median $1.04 million — strongly yields and Casa Delmar off-the-plan options.

• Manly Vale units: median $1.125 million —walking distance to Manly amenities at a discount.

• Queenscliff / Narrabeen units: median$1.21–$1.34 million — beachside with 3%+ yields.

Tip: The First Home SuperSaver Scheme lets you voluntarily contribute up to $50,000 into super and withdraw it for a deposit, potentially saving thousands in tax. Pair this with a well-structured home loan, and you can meaningfully shorten the savings timeline.

Refinancing: what Northern Beaches homeowners should check in 2026

If you took out your current home loan before mid-2022, there’s a strong chance you’re paying a “loyalty tax” — lenders routinely price new customers more sharply than existing ones. With many Northern Beaches suburbs having added 30–50% to equity over five years, you may also have room to:

• Refinance onto a sharper rate and potentially capture cashback offers

• Restructure into an offset account to reduce interest without locking up capital

• Release equity for a renovation (particularly relevant as updated local DCPs make additions more straightforward) or an investment property

• Consolidate higher-rate personal debt into a single,lower-rate facility

Mortgages Plus runs a free rate review on existing loans - we benchmark your current rate against more than 30lenders on our panel and provide a written comparison within 48 hours.

Investor outlook: yields, vacancies and rent growth

The Northern Beaches rental market remains exceptionally tight. Across the LGA, vacancy rates sit below 1%in almost every suburb we track, and weekly asking rents rose 3–22% over thepast 12 months. Standout rent growth came from:

• Beacon Hill houses: +22% to $1,350 per week

• Fairlight units: +17% to $1,050 per week

• Cromer houses: +13% to $1,300 per week

• Mona Vale units: +13% to $850 per week

• Forestville houses: +11% to $1,200 per week

Best gross yields (>3.5%) are currently in Brookvale, Manly Vale, Narrabeen, Queenscliff, Freshwater and DeeWhy units — the combinations of sub-$1.5 million price points and sub-1% vacancy are where most of the positive-cashflow-friendly opportunities sit.

One important note forinvestors: the 2017 federal depreciation rules restrict Plant and Equipment(Division 40) deductions on second-hand residential property, but structuraldepreciation on brand-new stock remains generous. If you’re weighing new buildversus established, factor this into your after-tax return calculations.

Major projects that could move prices 2026–2030

Sources: Northern Beaches Council, Transport for NSW, Hotspotting Location Report (Jan–Apr 2026).

How Mortgages Plus helps Northern Beaches buyers

We’re a local brokerage that lives and works on the Northern Beaches. That means we know which lenders are comfortable with Manly apartment blocks, which value Frenchs Forest off-the-plan product sensibly, and which private banks compete hardest for loans above $3 million.

• Local expertise: every broker on our team has written Northern Beaches loans for more than five years

• 30+ lender panel: from the big four to credit unions, non-banks and private banks

• Free borrowing assessments: we benchmark your capacity across multiple lenders before you fall in love with a property

• Free rate reviews: annual check-ins to make sure your loan still stacks up

• Pre-approval in days: we prioritise fast turnaround for competitive Saturday auctions.

Talk to Mortgages Plus about your Northern Beaches purchase today. Nobligation, and the first meeting is always free

Frequently asked questions

What is the median house price on the Northern Beaches in 2026?

Across the 24 most-traded Northern Beaches suburbs, the median house price ranges from $2.1 million in North Narrabeen to $5.01 million in Balgowlah Heights. The whole-of-LGA medians around $2.73 million, with most suburbs delivering 7–9% average annual growth over the past five years.

Which Northern Beaches suburb is the most affordable for first-home buyers?

For unit buyers, Brookvale ($1.0M), Dee Why ($1.04M), Manly Vale ($1.13M), and Avalon Beach ($1.17M) offer the lowest median prices. Brookvale and Dee Why are particularly popular with first-home buyers using the First Home Buyer Assistance Scheme, thanks to sub-$1.1Mpricing and strong rental yields.

How much deposit do I need to buy on the Northern Beaches?

A 20% deposit avoids Lenders Mortgage Insurance (LMI) but requires serious savings - around $200,000 for a $1 million unit and $540,000 for a $2.7 million house. Eligible first-homebuyers may be able to purchase with just a 5% deposit (no LMI) via the First Home Guarantee, subject to property price caps.

Is now a good time to buy on the Northern Beaches?

The Northern Beaches is a long-term, supply-constrained market. Short-term medians can move either way - Avalon Beach dropped 8% in the past year while Balgowlah Heights rose 19% - but five-year growth has averaged 7–9% in most suburbs. Timing individual suburbs matters less than securing a property aligned with your borrowing capacity and holding it through a cycle.

What are the best investment suburbs on the Northern Beaches in 2026?

For yield, Brookvale (4.0%), DeeWhy (3.9%), Freshwater (3.6%), and Manly Vale (3.6%) units lead the LGA. For capital growth momentum, Frenchs Forest, Mona Vale, Killarney Heights, and Fairlight stand out - all recorded double-digit growth over the past 12 months or are set to benefit from major infrastructure and rezoning.

Can I use equity in my Northern Beaches home to buy an investment property?

Yes. If your current NorthernBeaches home has appreciated substantially (five-year growth averaging 7–9%across most suburbs has built significant equity for owner-occupiers), you can often release 80% of the revalued property’s value, less the existing loan. Mortgages Plus can structure the additional facility separately to keep your lending tidy and preserve tax deductibility.

How will Frenchs Forest’s rezoning affect property prices?

Frenchs Forest is an NSW Government Priority Planned Precinct with 2,000 new homes, a new town centre,$500 million in road upgrades and the $2.1 billion hospital precinct over the next two decades. Infrastructure-led corridors historically outperform; Frenchs Forest house prices rose 7% in the past year and have averaged 9% over five years.

Does Mortgages Plus charge for its services?

No. As with most Australian mortgage brokers, we’re paid by the lender you ultimately choose, not by you. You get access to more than 30 lenders, personalised advice and ongoing support at no cost. We’re required by law to act in your best interests.

Speak to a Northern Beaches mortgage broker today

Whether you’re eyeing a Brookvale unit for your first home, a Frenchs Forest family house, or a Manly Harbourside upgrade, the right home loan structure can save you tens of thousands over the life of the loan. Speak with Mortgages Plus on 0447 222 628 or contact us to book a free, no-obligation chat.